A Lyft crash doesn’t feel unusual at first. Cars pull over. Phones come out. Insurance questions start almost immediately. Then someone asks the question that actually matters: who pays for this?

In Florida, the answer after a Lyft accident is rarely simple. Payment depends on timing, insurance layers, and which policies are triggered first. This guide focuses on insurance mechanics only—not legal strategy, not payouts—so you can understand how payment typically works after a Lyft accident.

Why Payment Isn’t Always Obvious in Lyft Accidents

In a normal car crash, there’s usually one driver and one insurance policy to start with. Lyft accidents don’t work that way.

A single rideshare crash can involve:

- The Lyft driver’s personal insurance

- Lyft’s commercial insurance

- Another driver’s insurance

- Your own auto policy

- Your health insurance

Which one pays first depends on what the Lyft driver was doing at the exact moment of the crash, not just who caused it. That’s why rideshare accidents feel confusing so quickly—there isn’t one automatic answer.

Florida PIP Coverage: What Pays First

Florida is a no-fault state. That means Personal Injury Protection (PIP) usually pays first after a car accident, including Lyft accidents.

PIP typically covers:

- A portion of medical bills

- A portion of lost wages

PIP applies regardless of who caused the crash and is often the first source of payment for treatment. However, PIP is limited and doesn’t cover everything, which is why additional insurance layers become relevant in rideshare accidents.

This is where Lyft’s insurance structure comes into play.

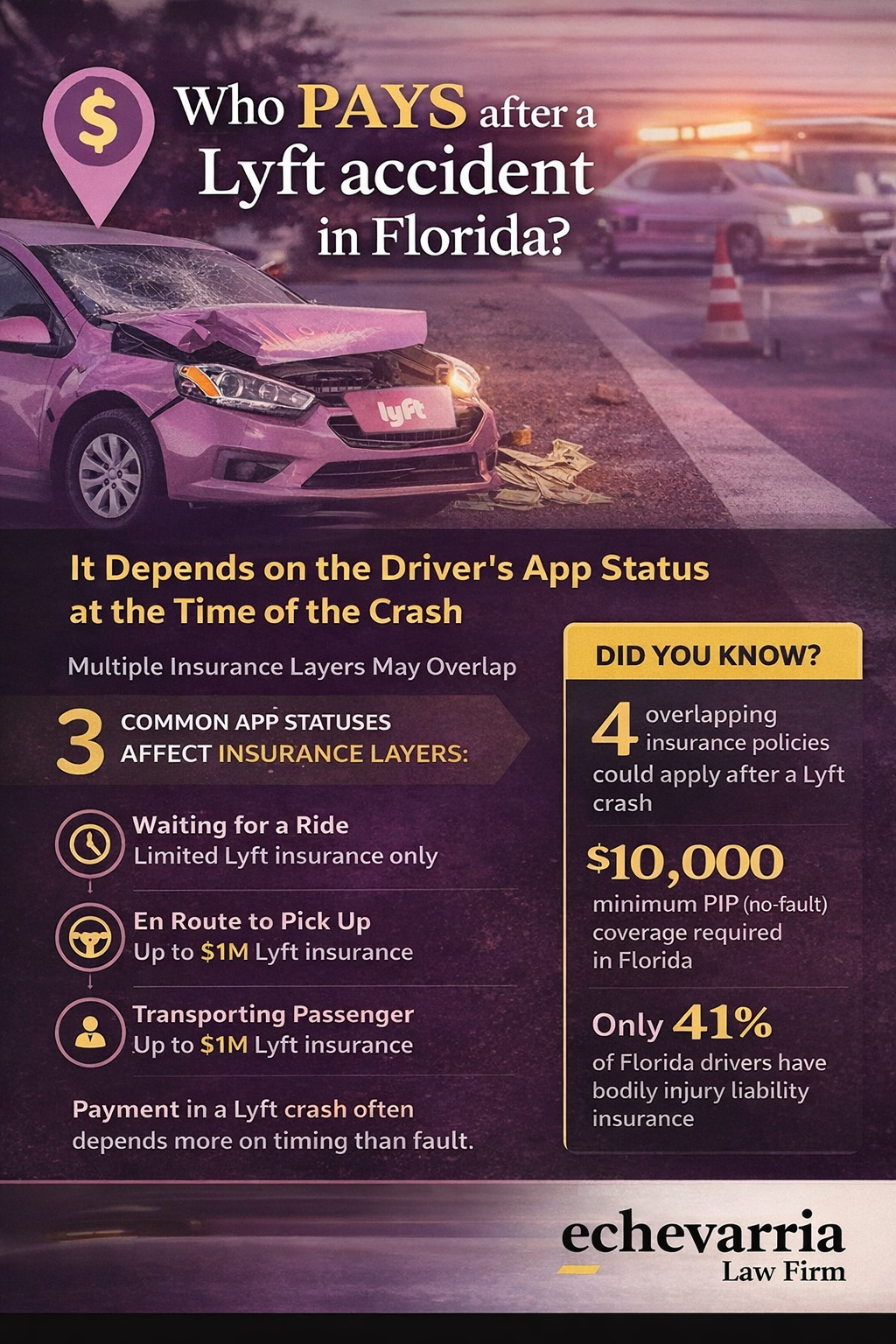

Lyft’s Insurance Coverage Explained in Plain English

Lyft provides different levels of insurance coverage depending on the driver’s app status at the time of the crash. This isn’t about blame—it’s about timing.

Driver Is Off the Lyft App

If the driver is not logged into Lyft:

- Lyft’s insurance does not apply

- The driver’s personal auto insurance is responsible

At this point, the accident is treated like a standard car crash.

Driver Is Logged In, Waiting for a Ride

If the driver is online but hasn’t accepted a ride yet:

- Limited Lyft insurance may apply

- Coverage is lower and more restrictive

- Personal insurance may still be involved

This phase often creates confusion because coverage exists—but it isn’t the same as full rideshare coverage.

Driver Is En Route or Transporting a Passenger

If the driver has accepted a ride or is actively transporting:

- Lyft provides higher commercial insurance coverage

- Coverage can include up to $1 million, depending on the situation

This is the phase most people think of when they imagine “Lyft insurance,” but it only applies during active ride periods.

When Multiple Insurance Companies Are Involved

Lyft accidents often trigger overlapping insurance responsibilities, which can slow everything down.

Commonly involved insurers include:

- The Lyft driver’s personal auto insurer

- Lyft’s commercial insurer

- Another driver’s insurer (if multiple vehicles were involved)

- Your own PIP provider

- Health insurance providers

When several insurers are involved, payment questions don’t always get resolved quickly. Each company may wait for confirmation about app status, coverage priority, or documentation before paying.

Common Situations That Create Payment Disputes

Certain scenarios make payment issues more likely after a Lyft accident:

- Unclear app status at the time of the crash

- Gaps between personal and rideshare coverage

- Disagreements between insurers about who pays first

- Delayed reporting of the accident

- Missing documentation, such as ride screenshots or timestamps

None of these situations mean payment won’t happen—but they often lead to delays and back-and-forth between insurance companies.

Why Early Information Matters More Than People Realize

In Lyft accidents, early details matter more than people expect.

Information that often becomes critical includes:

- Screenshots showing the ride was active

- Accurate timestamps

- Medical records tied closely to the accident

- Consistent reporting across insurers

Insurance decisions are frequently based on what’s documented early, not what’s remembered later. That’s why understanding the insurance structure from the beginning can reduce confusion as the process unfolds.

Where This Fits in the Bigger Picture

This article is meant to explain who typically pays after a Lyft accident—not to replace deeper discussions about rideshare cases.

For a broader overview of how Uber and Lyft accidents are handled in Florida, see our page on Uber and Lyft accidents and how rideshare crashes differ from ordinary car accidents.

One-line takeaway

After a Lyft accident in Florida, payment depends less on fault and more on timing—specifically, the driver’s app status and which insurance layers are triggered first.